Niche Product Marketing – Part 1 – The “Why”

Amongst life and health insurance general categories, one can find niche sub-groupings of products that are extremely useful to the consumer and can be very profitable to the producer when one knows how and why to properly market and prescribe them.

Although commonly considered outliers, niche products serve a masterful purpose in the greater market. Most were designed to complement or fill coverage gaps in more mainstream product lines. They are used to supplement or even replace what can’t be found or acquired from “traditional” domestic carriers, and they answer serious financial protection needs.

Niche products are not usually a primary consideration for the basic coverage needs of your clientele, but when an obvious solution isn’t readily available or when additional coverage is needed, niche product lines can serve your clients well and succinctly fill the dangerous holes in their life and health benefits.

So, the questions arise, why should you make the effort to market niche products? Why do your clients need these insurances that your domestic carriers don’t provide? The answer is that your clients are human beings, and nature and desire have made them fallible. Not everyone fits the mold set-out by standard-carrier underwriting and actuarial departments. I can bet that at one time or another, you have come across a prospect that is too fat, too old, too many health issues, drinks too much, makes too much money, makes too little money, works overseas, skydives or did cocaine the weekend before an insurance exam. I expect that you can identify with having to deal with some of those underwriting issues among your clientele, and I see those and similar issues day in and day out. Millions of Americans, your prospects, face these common insurance roadblocks, and prejudicial company standards keep them from purchasing the financial protections they need. And for that reason, the specialty, niche-product markets exist and flourish to this day.

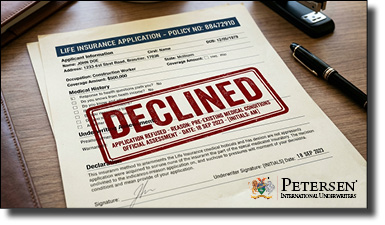

Your first step as an interested and dutiful insurance broker is to identify potential prospects for niche products. That part is easy. Any client that you have gotten quotes for or taken through underwriting but has been declined by an insurance company for basic or supplemental personal or corporate insurance of any kind is a ripe and ready candidate for a niche product. Those who are underinsured in life or disability coverage as well as those who have missed Medicare enrollment windows are all perfect prospects. In the specialty markets, you will be able to find niche products for most lines including life, medical and disability cases.

So now you are finding solutions for cases you thought were “dead in the water” so to speak. The niche market will make you a hero and won’t send you back to your clients empty handed even if your clients work on oil rigs, have severe depression, play professional basketball or have multiple sclerosis. The niche-product market is the “yes man” in a room full of naysayers. It’s a very exciting aspect of the insurance industry.

No matter how hard you work, no matter how many hours you put into a case, a declined case doesn’t pay a commission. Niche products do provide commissions upfront and on renewals. You can also double-up on compensation when prescribing supplemental policies on-top of fully-underwritten base-line coverage – two commissions while piggybacking the underwriting requirements of two carriers, simplifying the policy issuance and lessening your workload. It’s a win-win situation.