The Importance of Supplemental DI In Today’s Evolving Market

It’s a great time to be in the business of disability insurance, especially from an advisor, broker or consumer perspective. Foreign and domestic markets have been softening for some time now and many carriers and underwriting outlets lately seem to be fighting for DI dollars, willing to write for gross premium volume in the short run rather than the historical focus on long-term product profitability.

Furthermore, wholesale competition is rampant, and the issue and participation limitations of American companies are generally increasing. Despite the inflationary environment we are all experiencing in this country, disability insurance rates have mostly plateaued, if not receding in recent years.

Modest pricing for most occupation classes, combined with greater underwriting allowances and tech-driven allocations by insurers have brought renewed excitement to the market and more bang for your buck for consumers. Many carriers are moving to simplified issuance, streamlined underwriting platforms, using AI engines to review medical records and shuttering typical mainstay requirements like applicant physical examinations and blood and urine testing.

Although at first glance the evolving domestic and international DI markets appear to be in a progressive state, some serious antiquated underwriting methodologies and consumer-related limitations still exist. DI coverage gaps are persistent, and underinsurance is always a major problem of the health insurance industry.

Today’s economists remain in agreement with the great financial minds of the early twentieth century, who through decades of study and practice declared that at least 65% of one’s income is necessary to maintain some semblance of personal and familial lifestyles, including basic needs for living. 65% of income insured is the magic number and when considering the taxation of employer-paid group benefits, 75% is even more appropriate when available.

For many working Americans, acquiring such levels of income protection through insurance is possible with group long-term disability (LTD), government-sponsored benefits and individual DI plans or some combination thereof. But for many in this country, those options alone won’t cut it.

In the realm of disability insurance, there remains great financial prejudice against high income earners which continues to this day through the guidelines and limitations of most U.S. insurance companies. Anyone in the private sector, mostly gray and white collar, making over $250,000 per year will typically be insufficiently insured without the use of supplemental or excess DI benefits.

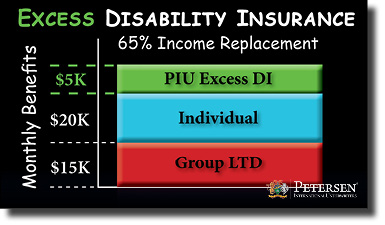

A great example of the economic disparity that many high-net-worth clients face is the lack of enough income protection. Let’s take a physician or a successful attorney for example, making north of $750,000. With years of hard work, ambition, natural talent and maybe a bit of luck, he/she has been able to achieve and maintain a prosperous career, earning a significant income that demands attention and protection. An advisor worth their salt prescribed personal DI and was able to get their client approved for $20,000 of monthly benefit on top of an underlying $15,000 per month of group LTD that was paid for by the client’s employer. Wow, $35,000 of monthly disability benefits. That sounds like a lot of coverage, but if you really look at it, $35,000 is not enough for the client in question. That monthly benefit equates to only 56% of his/her income.

If I told you that tomorrow you would fall victim to a debilitating accident or illness and that your income would suddenly be reduced by 44%, you might have a problem with that. Consider your life, your lifestyle, your family, your home, your bills and expenses. Could you maintain a semblance of your current situation with only 56% of your income?

Further consider that the client in question must pay taxes on those group LTD benefits. Now what? The client’s 56% is looking more like 48% or 50%. Underinsurance can be a great travesty, making supplemental DI programs all the more important.

You could argue that 50% of $750,000 is a heck of a lot more money than what most Americans make or live comfortably on. Someone with that level of income may also have significant assets, liquid or otherwise that could potentially stave off financial ruin. But the point of disability insurance is to preserve accumulated assets. So, why should a high-net-worth individual be penalized for making more money and be pressured to demolish their holdings and legacy potential in order to survive? A wealthy client needs more income protection for the simple truth that they have more to lose at the hands of disablement.

Supplemental DI benefits are available in the domestic disability market, but such coverage is more common and robust with higher limits in the specialty international markets like Lloyd’s of London. Individually underwritten programs are traditionally how one would acquire excess disability benefits. But in the last decade, a strong push for simplification of employee benefits platforms gave rise and evolved to group and multi-life guaranteed-issue (GSI) disability products.

Employers with partners or personnel making in excess of $250,000 without sufficient income protection are candidates for a supplemental GSI disability program. Most GSI products provide group discounts, guaranteed-issue underwriting, uncomplicated online enrollments, coverage portability and voluntary benefit increases.

Supplemental disability benefits serve many purposes in the market, including breaking through prejudicial issue and participation limitations that are regularly encountered by high income earners. Excess DI also allows employers to add value by contractually providing high-limit benefits, helping acquire and retain marquee personnel. The standard disability market often demonstrates a diminutive appetite for robust benefit levels, making the addition of supplemental DI benefits very important to working Americans.

–Published with permission from Aspire Magazine.