Layering Personal Disability Policies

Without financial protection of one’s paycheck, a person stands to lose their single most vital source of economic freedom. Income provides for the necessities for one’s family – it pays for food, shelter, transportation, education, healthcare and all of the other bills and costs the average American encounters on a daily basis. It also allows for the luxuries and niceties that we often take for granted. But it is fact that most Americans making up today’s workforce are insufficiently covered by some form of income protection insurance.

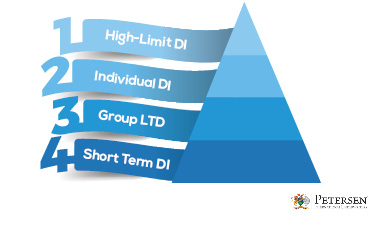

Please let me remind you that the proper prescription of DI entails a layering approach of multiple insurance policies. Income protection isn’t black and white. There usually isn’t one simple solution. There are actually three levels of disability insurance, and all three can be extremely important to your clients.

The first layer is group insurance better known as LTD (long term disability). Many U.S. corporations provide small layers of mandatory or voluntary guaranteed-issue group LTD benefits. Since the carriers of such plans offer terms on a guaranteed basis, underwriter guidelines will commonly limit benefits to 50% to 60% of income with usual caps of $5,000 to $15,000 per month. For the majority of blue-collar and governmental employees, employer-sponsored group insurance combined with state disability benefits provides acceptable income replacement coverage. But most of the workforce in this country are employed by small business owners, are self-employed or are independent contractors. In these instances, group disability insurance is oftentimes not available or isn’t sufficient on its own.

The second layer of income protection is IDI (individual disability insurance). Those without group DI or without a sufficient level of group DI can seek individual disability insurance from a handful of large, reputable U.S. carriers. These insurers employ individual underwriting and morbidity analysis to provide prospects with policies similar in comprehension to group LTD certificates. Most Americans can find acceptable levels of disability coverage from a combination of group and standalone individual benefit sources.

However, there are many income-earners in this country that have salaries in ranges that cannot be effectively covered by group and/or standard individual disability policies. That brings us to the third layer of DI. Most in the white-collar market as well as physicians, and many in the rapidly-expanding grey-collar market have annual earnings that can hardly be insured by such a combination of group insurance and a single, traditional disability income policy. The third tier is comprised of high-limit DI and is only accessible through the Surplus Lines market which specializes in providing income protection above the usual disability benefit limitations of most U.S. carriers. High-limit or “excess” disability insurance is readily available on a fully-underwritten individual basis as well as for groups large and small on a multi-life guaranteed-issue basis.

For moderate to high-net worth individuals, the risks of underinsurance can prove to be severe and financially disastrous. Your clients need to understand the importance of the three layers of income protection, and with your guidance, properly tier supplemental benefits on top of existing group and/or individual policies. Safeguarding 50% of one’s income is not enough. Safeguarding 60% of one’s income is not enough. The three-layer benefit approach to disability insurance will successfully fill the subtle and blatant gaps in your clients’ risk exposure.